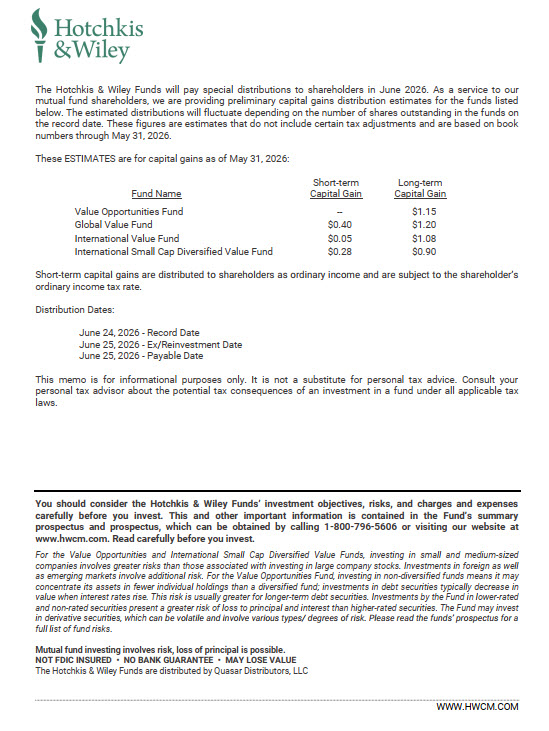

AI-driven disruption to application software is a topic that often comes up with our clients. Workday, one of our largest holdings, offers an example of how we think about the investment opportunity.

Like other investors, we’ve been impressed with the pace of innovation in AI. Today, the consensus view among investors is that AI could prove to be a significant headwind to incumbent software vendors, and the stocks of publicly traded software firms have sharply de-rated to reflect this increase in perceived risk.

While our research team thinks many software vendors could be negatively impacted by AI, we think the impact will vary widely depending on the company. We believe the software products that are most threatened by AI are those that are loosely integrated, lightweight point solutions. These software products are easy to install, easy to replace, and are often sold on short contracts or on a monthly subscription basis. At Hotchkis & Wiley, we have always assigned low-quality risk scores to these types of companies and we have avoided investing in them.

We believe Workday is very different. Workday is a deeply embedded, mission-critical system used by large, complex enterprises to run their core Human Resources (HR) and finance workflows. These are business processes that cannot fail and are closely scrutinized by regulators and auditors. Abandoning Workday would mean remapping years of configurations, absorbing significant switching cost, and accepting the risk of breaking core HR, payroll, or finance processes. Large enterprises are generally risk averse and they are extremely hesitant to replace core back-office systems of record like these.

The AI Bear Case Viewed Through Workday

The prevailing application software bear case has four main parts, but each looks very different for Workday than for a fragile, point solution software business.

First, as code gets cheaper to produce, investors worry about increased competition, both from new startups and from enterprises building their own software. We agree code is getting much cheaper to produce, but writing code has never been the hardest part of building a scaled enterprise software business. To quantify this, research and development (R&D) has been roughly half of Workday’s cumulative operating expenses to date. Only a portion of R&D employees at software firms are actually writing code, and only a portion of a developer’s time is spent coding. So while AI coding tools are driving R&D productivity gains, they do not dramatically change the overall cost structure of software startups or custom enterprise builds. Outside of R&D, sales and marketing capabilities remain as important as ever. Strong customer relationships, brand, and distribution partnerships take decades to build at scale. Meanwhile, cheaper code development helps Workday develop new functionality that it can cross-sell to its sticky installed base, which could be a meaningful tailwind to revenue growth.

Second, investors worry that AI agents will replace white-collar employment, reducing seat-based revenue streams. AI-driven layoffs have not yet appeared in broad employment data. However, if headcount pressure does eventually emerge, Workday has several important offsets. The company is currently shifting from mostly seat-based pricing toward a mix of consumption and seat-based pricing. Also, Workday’s multi-year contracts include inflation-based price escalators for most customers, so customers pay more each year even with flat headcount. Customers also often lose important discounts if they reduce the size of their contracts upon renewal.

Third, AI is changing the way users interact with software and could weaken moats built on user interface familiarity. This matters a lot for personal productivity and creative tools, but Workday’s moat has never been its user interface. In fact, one of the most common customer complaints is that Workday can often be cumbersome to use. For Workday, AI is an opportunity to improve this user interface weakness with new prompt-based navigation and agentic workflows that connect to common collaboration tools like Slack and Microsoft Teams. A more intuitive, AI-driven user interface could actually increase usage of Workday, a trend recently highlighted by application software peer Salesforce on its Q1 2026 earnings call.

Fourth, the most existential concern is that an agentic orchestration layer will be installed above HR and financials software, moving business logic into that layer and reducing incumbents to “dumb databases.” For lightweight solutions, we agree this is a genuine risk. For Workday, we are less concerned. Core HR, payroll, and the general ledger must be correct 100% of the time. Probabilistic AI models are not appropriate for this use case. For Workday, we think an agentic future is actually a positive, not a negative. Workday can monetize new agentic workflows through first-party agents and can monetize third-party agentic access to its systems of record via consumption pricing and API tiering. For enterprise-grade AI agents to produce real value, agent harnesses need access to accurate, up-to-date context, and much of this context for the back-office lives inside Workday. To date, evidence suggests that this context is not leaving Workday’s systems. Workday’s gross revenue retention remains at the high end for enterprise software at 97%, and our conversations with customers and consultants suggest Workday clients are firmly committed to Workday’s systems. Workday also continues to attract new customers. In Q1 of 2026, net new business drove 40% of Workday’s subscription revenue growth. Customers, including highly sophisticated AI labs like OpenAI, Anthropic, and Google, continue to sign new contracts with Workday, a signal Workday is still viewed as an important part of enterprise IT architectures.

How We Frame Risk

For every company we own, we weigh valuation and risk together. We measure risk through our fundamental risk rating framework that considers balance sheet, business quality, and governance. Workday performs well on that scale. It has a net-cash balance sheet and a strong cash flow profile. The business is high quality with sticky customers, revenue growth well above the broader economy, improving trends in net new bookings, high incremental margins, and an oligopolistic position at the high end of the enterprise market. Governance has been a risk we have watched closely, but the trend is positive. Although stock-based compensation is high, it has come down over time and the buyback has grown. In Q1 of 2026, repurchases reduced the share count by an impressive annualized rate in the mid-teens. On M&A, the company’s growth strategy remains organic-first, consistent with co-founder and CEO Aneel Bhusri’s view that enduring companies are not built through large acquisitions.

How We Think About Value

We think Workday offers limited downside and meaningful upside. Our valuation work starts with the downside; we always ask ourselves how much we could lose if we are wrong. In our discounted cash flow model, Workday’s current share price implies punitive outcomes that include mid-single-digit terminal revenue declines five years out and margins that are similar to other scaled enterprise software incumbents. These assumptions are worse than our downside case. If Workday does face a future of terminal decline like this, we think its margin could be much higher. Financial buyers routinely operate mature, deeply embedded software businesses in run-off mode at operating margins in the mid-60s% or above, not the high-30s%.

The backlog lens is even simpler. Workday’s remaining performance obligations — contracted revenue due even if the company signs no new business or any renewals — exceed its enterprise value. In a run-off scenario, simply collecting the gross-profit stream from existing backlog would make the current stock price roughly fair after considering the roughly offsetting impacts of time-value-of-money and net operating losses. By comparison, other incumbent application software peers trade at multiples of backlog, which implies a healthy slug of terminal growth. In Q1 of 2026, Workday’s backlog grew in the low-teens and the share count declined at an annualized rate in the mid-teens. This means the run-off value on a per share basis grew well in excess of 20%. While there is no guarantee these trends will continue, companies trading near liquidation value rarely enjoy this kind of value-per-share growth. Signs point to this growth continuing, with management flagging Q1 of 2026 as the best first quarter of net new bookings growth in five years, and the potential for net new bookings growth to accelerate in coming quarters.

While the downside is limited in even highly punitive downside scenarios, upside could be substantial. Our base case forecast assumes low-double-digit revenue growth for the intermediate term, gradual maturation toward GDP-like growth over the longer term, and a normal margin profile similar to large public software incumbents. Using these assumptions in our discounted cash flow model gets us to at least a double and plausibly a triple from today’s stock price. More optimistically, if Workday’s agentic opportunity scales and revenue indeed accelerates at high incremental margins, fair value becomes an even larger multiple of today’s stock price.1

Conclusion

While all software is not created equal, AI is more likely a tailwind than a headwind to Workday. Workday has demonstrated strong customer retention, long contracts, a mission-critical role in HR and finance workflows, a credible agentic strategy, improving governance, and a valuation that already discounts extreme disruption. In our view, Workday stands out as one of our best ideas, given its low valuation and attractive risk profile.